You want to sell your Greenbrae home and buy again in Marin without moving twice or missing the right next place. The puzzle is timing your sale, financing your purchase, and negotiating terms that protect you. With a clear plan, you can line up both transactions and move once, even in a market where speed varies by price tier.

Below, you will see how to map your timeline, choose the right financing tool, and use proven terms like rent-backs to bridge the gap. You will also find school and tax dates worth flagging early. Let’s dive in.

Greenbrae market reality

Greenbrae sits inside a high-end Marin market with single-family prices often in the high $1 million to low $2 million range. Condos run lower, and some pockets closer to Kentfield trend higher. Inventory is tight by historical standards, so well-prepared homes still sell. What varies is the speed, which depends on price, presentation, and strategy.

Price tiers and pace

- Condos and attached homes often transact between roughly $800,000 and $1.1 million. These can move in weeks when priced and staged well.

- Mid-tier single-family homes in Greenbrae commonly sit in the $1.5 million to $3 million band. Expect a wide days-on-market range. Well-positioned listings can go in 2 to 6 weeks, while others take 8 to 12 or more.

- Upper tier above $3 million can take longer due to a smaller buyer pool.

The takeaway: match your plan to your price tier. If your segment tends to move slowly, you will want extra buffer or a financing tool that buys time.

How long it really takes

For many Marin transactions, the period from listing to accepted offer plus escrow often totals about 2 to 4 months, with luxury listings taking longer. Typical escrow for financed purchases is about 30 to 45 days, and delays can occur with appraisal, underwriting, or title. Build your schedule by adding your submarket’s likely days on market to a 4 to 6 week escrow. If you want a single move, you can back into a list date that lands your close in your preferred window.

Choose your move strategy

There are three common paths to sell in Greenbrae and buy again in Marin. Your choice depends on your risk tolerance, cash flow, and the competitiveness of your target segment.

1) Sell first, then buy

You list, accept an offer, and close. With proceeds in hand, you shop for your next home and write a strong, non-contingent offer. This is the most conservative from a financial standpoint. The tradeoff is you might need short-term housing if you have not yet secured your next property. You can reduce that risk by negotiating a rent-back on your sale.

2) Buy first with a bridge or HELOC

You secure temporary financing, purchase your next home, then sell your current one and repay the short-term loan from sale proceeds. This can help you write a competitive, non-contingent offer in a tight submarket. The cost and risk are higher since you may carry two payments for a period. A detailed cost and timing model is essential.

3) Sell, then rent back while you buy

You close on your sale, remain as a short-term tenant under a rent-back, then move once your purchase closes. This combines financial clarity from your closed sale with a single move. It requires clean rent-back terms and coordination with the buyer’s lender and insurer if the stay is extended.

Financing tools explained

Short-term financing fills the gap between sale proceeds and your next purchase. Understand the basics before you choose.

Bridge loans at a glance

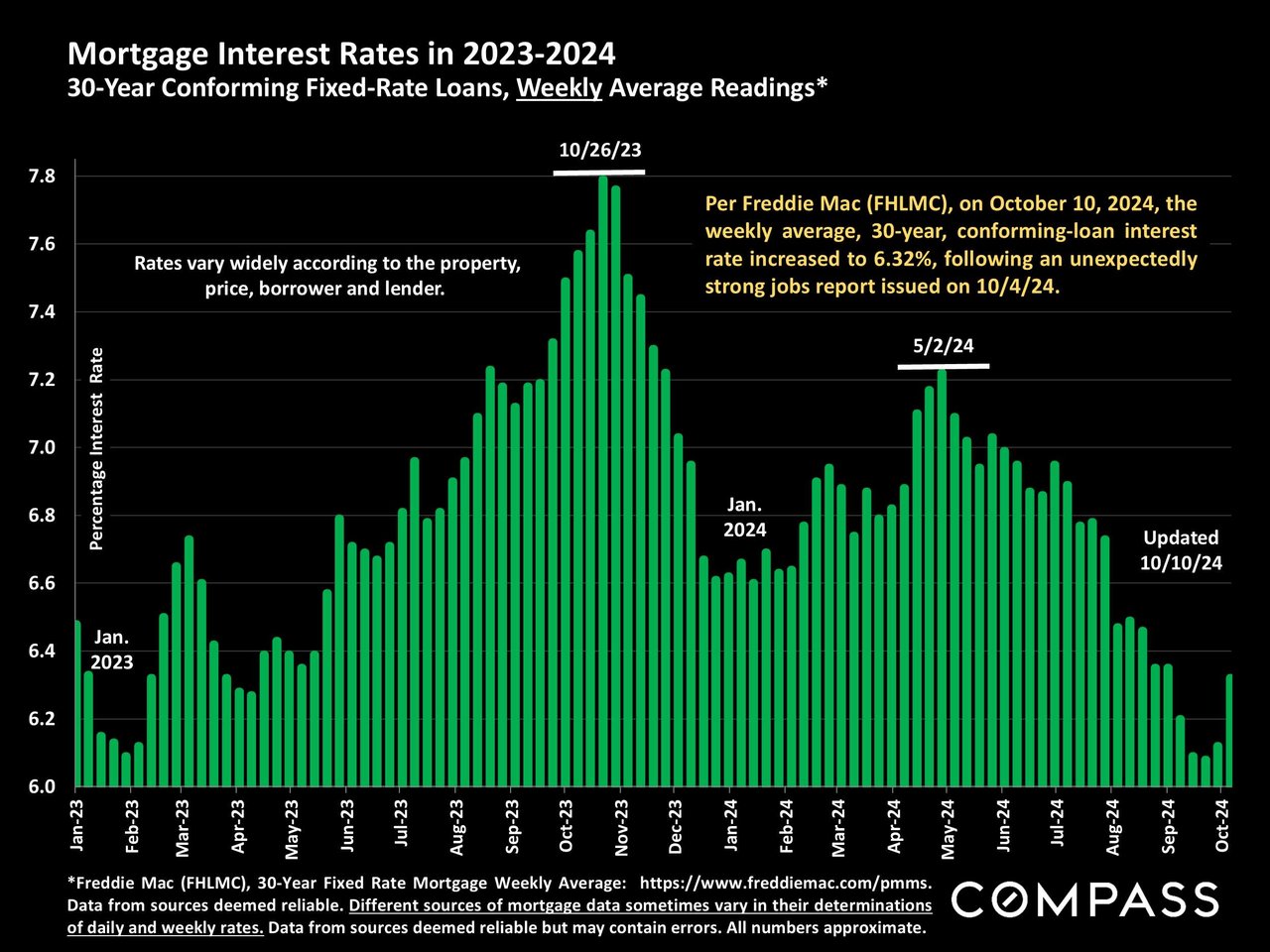

A bridge loan is a short-term loan, often interest-only, that covers your down payment or even the entire purchase price so you can buy before you sell. Typical terms run 3 to 12 months, with higher rates and fees than long-term mortgages. Lenders generally expect solid equity, strong credit, and the ability to carry two payments for a period. For a clear, consumer-friendly overview, review this explanation of how bridge loans work from Bankrate.

When a bridge makes sense: you have meaningful equity, you need to write a non-contingent offer to win a specific home, and you have a conservative plan to repay within the loan term.

Bridge loan checklist:

- Get written conditional approval, not just a conversation.

- Confirm payoff mechanics at sale and any prepayment fees.

- Verify lien position and whether the loan cross-collateralizes your properties.

- Stress test your plan if your sale runs 30 to 60 days longer than forecast.

HELOC, cash-out refi, and piggyback options

A home equity line of credit or home equity loan can be a lower-cost alternative to a bridge loan, though terms vary and some lenders limit new HELOCs on listed properties. A cash-out refinance can unlock funds but changes your long-term mortgage and often takes longer. Some buyers also use an 80/10/10 structure to reach a larger down payment while avoiding mortgage insurance. For a plain-English comparison of bridge loans and HELOCs, see this overview from Rocket Mortgage.

Negotiating when you still own

If you prefer to buy with a sale contingency, understand how sellers evaluate that risk and how to make your offer more acceptable.

- Sale contingency with kick-out: the seller can continue to market the property and accept a stronger offer. You then have a short window, often 24 to 72 hours, to remove your sale contingency or step aside. Expect to show evidence that your current home is listed or under contract.

- Make it stronger: shorten contingency windows, increase earnest money, and show clear proof of your sale progress. Clear communication can help a seller say yes.

On the sale side, a rent-back is a powerful lever when you want a single move.

- Rent-back basics: the buyer closes and you stay on as a short-term tenant, commonly 30 to 60 days, sometimes longer with lender and insurer approval. Spell out daily or monthly rent, a security deposit, utility responsibility, insurance requirements, a firm move-out date, and holdover penalties. Long stays can create mortgage or insurance issues for the buyer, so document everything clearly.

Plan around schools and taxes

If you want to avoid a mid-year transfer, build your closing targets around local school calendars and your expected escrow period.

Set summer targets

Families in Greenbrae often look to the Kentfield School District and Tamalpais Union High School District calendars when planning a summer move. You can reference the Kentfield School District calendar for current year dates. The Tamalpais Union High School District shows a late August start and mid-June finish pattern, as reflected in the 2025–26 calendar on EduCounty. If you want a single move with no mid-year disruption, aim to close and move before the August start for the year you are targeting.

Practical planning tip: set two models. A conservative plan has your sale close by mid-July, which adds buffer if escrow slips. An aggressive plan targets a late-August close, which is tighter if anything delays underwriting or appraisal.

Understand tax windows

- Primary residence exclusion: if you have lived in and owned your home for 2 of the last 5 years, you may qualify to exclude up to $250,000 of gain if single or up to $500,000 if married filing jointly. See the details in IRS Publication 523.

- California base-year and transfer rules: Proposition 19 updated parent-child exclusions and expanded tax base portability for eligible owners who are seniors or have disabilities. Review current guidance on the California State Board of Equalization’s Prop 19 page, and confirm forms and deadlines with the county assessor.

Always consult a qualified tax advisor if your gain may exceed the exclusion, if you have a rental history with depreciation to recapture, or if your occupancy history is complex.

Sample timelines you can use

Below are three example paths. Pick the one that best matches your priorities and the pace of your price tier.

Conservative: sell first, then buy

- List and go under contract: 2 to 8 weeks is typical for many mid-tier homes when well prepared. Luxury may take longer.

- Escrow: 30 to 45 days is common for financed buyers.

- Total: about 2 to 4 months from listing to vacate.

Pros:

- Lower financial overlap since proceeds arrive before your next purchase.

- Stronger purchasing position if you buy with cash or a large down payment after closing.

Tradeoffs:

- You may need temporary housing if you have not yet secured your next home.

- Market risk if your target segment moves faster than your sale timeline.

Aggressive: buy first with a bridge or HELOC

- Secure short-term financing approval and write a non-contingent offer.

- Close on the purchase, then sell your Greenbrae home and repay the short-term loan.

Pros:

- Highest competitiveness on your purchase.

- Move once if your sale aligns with your new-home close.

Tradeoffs:

- Higher carrying costs and rate or fee sensitivity.

- Exposure if your sale runs beyond your bridge term.

Hybrid: sell with a rent-back while you buy

- Close your sale, stay 30 to 60 days with a documented rent-back, then move once your purchase closes.

Pros:

- Proceeds in hand plus a single move.

- Clear occupancy terms that support planning around school start dates.

Tradeoffs:

- Requires careful documentation, including insurance and holdover terms.

- Longer stays may need lender or insurer approval for the buyer.

Prep your Greenbrae home to sell fast

Speed and certainty come from preparation. In a tight-inventory market, you want buyers to compete for your property quickly so your move plan holds.

- Price with data: align with your submarket’s recent sales and list-to-sale patterns.

- Make targeted improvements: paint, lighting, landscaping, and minor kitchen or bath refreshes can lift photos and first impressions.

- Stage for clarity: bright, neutral staging helps buyers see the space. Quality images and crisp copy drive traffic in the first week on market.

- Leverage project management: coordinating vendors, improvements, and calendar windows is what keeps your list-to-close on schedule.

If you want help funding strategic updates, ask about using Compass Concierge to advance the cost of pre-sale improvements that can raise price and shorten days on market. A design-forward plan, executed cleanly, puts you in control of timing.

Putting it all together

Selling in Greenbrae to buy again in Marin is very doable. Start with your price tier’s expected days on market, add a realistic escrow period, then choose the path that best fits your cash flow and timeline. If you need maximum purchase strength, explore a bridge loan or HELOC with a clear exit plan. If you value financial certainty and a single move, pair a clean sale with a well-written rent-back. Layer in school and tax dates early, and you will have a calm, one-move transition.

When you are ready to plan your sale, pricing, and pre-market improvements, reach out to Allison Salzer for a tailored timeline and strategy.

FAQs

How long does it take to sell a Greenbrae home and move out?

- Many Marin transactions run about 2 to 4 months from listing to closing, plus or minus based on your price tier and presentation. Escrow alone often takes 30 to 45 days for financed buyers.

What is a rent-back and how long can it last?

- A rent-back lets you stay after closing as a short-term tenant, commonly 30 to 60 days, with terms for rent, deposit, insurance, and a firm move-out date. Longer stays need lender and insurer approval.

Can I make a sale-contingent offer in Marin and still compete?

- Yes, but you may need tight contingency windows, strong earnest money, proof your home is listed or under contract, and acceptance of a seller kick-out clause that allows the seller to keep marketing.

How should I time my move around local school calendars?

- Target a summer close and move before the late August start. Confirm dates on the Kentfield School District calendar and the Tamalpais Union pattern shown on EduCounty.

What tax rules matter when I sell in Greenbrae?

- Review the primary residence exclusion in IRS Publication 523 and California’s Proposition 19 guidance from the State Board of Equalization. Consult a tax advisor for specifics.